In a groundbreaking development, the United States has witnessed an unprecedented surge in energy storage installations during the second quarter of 2023, as reported by the latest “U.S. Energy Storage Monitor” released by Wood Mackenzie and the American Clean Power Association (ACPA) on September 25, 2023. This quarterly achievement, totaling 5,597 MWh, not only marks a new record but also signifies a significant milestone in the nation’s commitment to transitioning towards a sustainable and resilient energy landscape.

I. The Grid-Scale Triumph

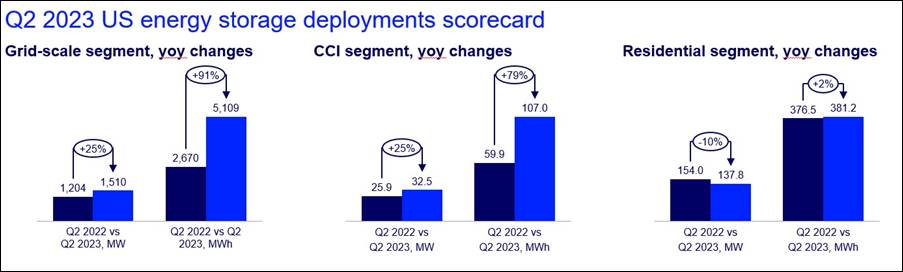

The star of this record-breaking performance is undeniably the grid-scale segment, which contributed a staggering 5,109 MWh in Q2, surpassing the previous record set in Q4 2021 by an impressive 5%. This segment also experienced an outstanding 172% growth quarter-over-quarter, showcasing the resilience and adaptability of the energy storage market. California emerged as a leader in this domain, contributing 738 MW and claiming a substantial 49% share of the installed capacity, further solidifying its position as a trailblazer in renewable energy adoption.

II. Market Dynamics and Projections:

US Energy Storage Developments Scorecard

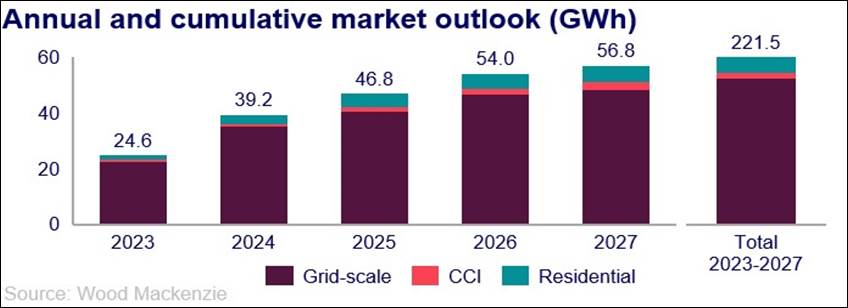

ACPA’s VP of Research and Analytics, John Hensley, emphasized the pivotal role energy storage plays in enhancing the grid and ensuring reliability. Despite facing challenges such as supply chain disruptions and interconnection delays, the market is poised to achieve nearly double the annual installations. Wood Mackenzie projects the grid-scale segment to be the primary driver, accounting for 83% of total installations or 55 GW in the five-year forecast from 2023 to 2027.

III. The Resilient Rebound and Unfulfilled Projections:

After experiencing consecutive quarterly declines, the energy storage market witnessed a remarkable rebound in Q2. Vanessa Witte, senior analyst with Wood Mackenzie’s energy storage team, attributed this rebound to the realization of delayed projects, primarily caused by supply chain issues. However, despite the record-breaking quarter, the projected pipeline did not fully materialize, with over 2 GW pushed back. This highlights the ongoing challenges within the industry that need to be addressed for sustained growth.

IV. Community, Commercial, and Industrial Installations:

Community, Commercial, and Industrial Installations

The community, commercial, and industrial (CCI) segment, with 107 MWh in installations, outperformed any quarter in 2022 but faced a 53% decline from the previous quarter’s substantial spike. Nevertheless, it maintains a commendable 25% year-over-year growth. The report indicates that, while the residential storage segment recorded a second consecutive decline at 381.2 MWh, California experienced a notable decline of 17% quarter-over-quarter and 37% year-over-year.

V. Future Outlook and Adjusted Growth Forecasts:

Despite challenges in the commercial and industrial segment meeting growth projections, the residential sector is projected to experience robust growth, reaching a total of 8.0 GW in 2027. Witte, however, acknowledged the need for a revised growth forecast for the CCI segment, downgrading it by 28% to 3 GW in the five-year outlook.

Conclusion:

The surge in energy storage installations during Q2 2023 showcases the resilience and adaptability of the U.S. energy market. As the nation aims to double annual installations and prioritize grid-scale solutions, it is crucial to address challenges such as supply chain disruptions to ensure sustained growth. The path towards a cleaner and more sustainable energy future seems promising, but strategic measures and collaborative efforts will be vital in overcoming obstacles and fulfilling the potential of energy storage in the United States.